Summer is a time of endings and beginnings. For most of the about 1.8 million people who just graduated from college, this season marks the end of at least 17 years of formal education and the launch of their careers.

My career started a little sooner than that.

My first real job was as a student organizer during my senior year at American University, in Washington. Right before I graduated two years ago, when I filed my tax return, I was surprised to learn that I owed an extra $1,200 on the less than $13,000 I earned.

Why did I owe the Internal Revenue Service so much? Because my employer misclassified me as an independent contractor, I owed self-employment taxes in addition to regular income taxes. And, because I had no idea I needed to pay these taxes every quarter, I owed a large lump sum that Tax Day.

It was a big wakeup call. As a 21-year-old soon-to-be college graduate majoring in economics, I was financially illiterate. Neither in college nor at top-ranked Wootton High School, in Rockville, Md., did I learn how to manage my money beyond making sure I could budget for the basics.

When I talk to my friends about those tax troubles, I find that their grasp of personal finance is just as poor or worse. While we might feel ready to start our careers after graduation, we’re woefully unprepared to look out for ourselves in the economy.

And we aren’t alone. A recent Financial Industry Regulatory Authority (FINRA) study showed that less than a quarter of millennials could correctly answer at least four out of five questions on a basic financial literacy quiz.

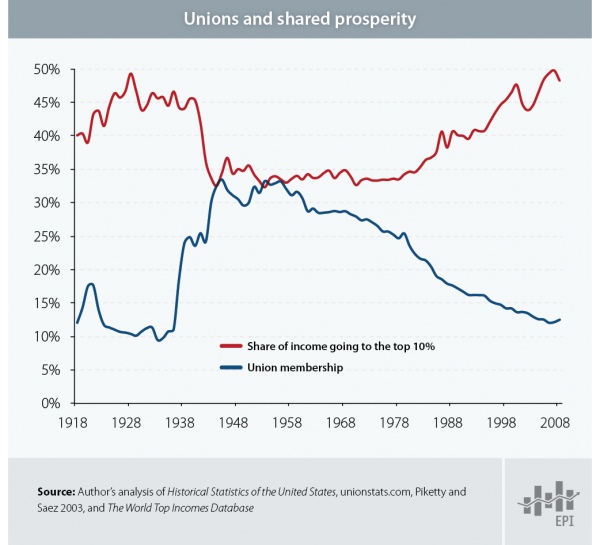

As the lackluster recovery from the Great Recession lumbers forward, personal finance matters more than ever. Some 53 million Americans — one in three working people — are freelancers. And according to software company Intuit, 40 percent of the workforce will be freelancing or working as an independent contractor by 2020. That’s a pleasant way of saying they lack job stability.

In the so-called gig economy, juggling multiple part-time or temporary jobs to make ends meet is commonplace. Unless they qualify for health care subsidies, people working in this sector pay for medical insurance completely out of pocket. If they manage to save for retirement, they have to do it alone.

Many millennials are learning the rules of the game as we’re playing it. But we’re actually a lot like our elders. The FINRA study showed significant rates of financial illiteracy among Boomers and Gen Xers as well.

The difference is that our generation faces a job market that’s nothing like the one our parents faced. Combined with the $1.2 trillion of student-loan debt currently owed, that means we need more financial smarts if we’re going to thrive in today’s precarious economy.

More public K-12 school systems across the country need to follow the example of states like Virginia by prioritizing students’ financial literacy and requiring a course in personal finance regardless of whether they’re college-bound or not. Everyone needs to know enough of the basics to fend for themselves.

Of course, if our nation’s employers took the high road and paid fair wages, provided health care and retirement benefits, and gave regular, reliable schedules, we wouldn’t have to rely so much on our own wits to get by. But if our bosses won’t look out for us, we have to look out for ourselves.

Many Millennials are struggling to pay our bills now, much less build a solid future. Just as I’ve had to educate myself financially, my entire generation needs to get up to speed on how the economy works (or doesn’t), so we can join together to make it more sustainable for everyone.